My Case for Keeping a Handwritten, Manual Budget vs Using an App for Your Budget

The title alone may keep most readers away. But if you’re like me and still prefer something a little more analog this post is a nod to you. I’ll share why a manual budget has been my steadfast approach for the past fifteen years, and why it’s a tried-and-true method worth considering if you’re over data sharing apps and excel spreadsheets just don’t speak to you.

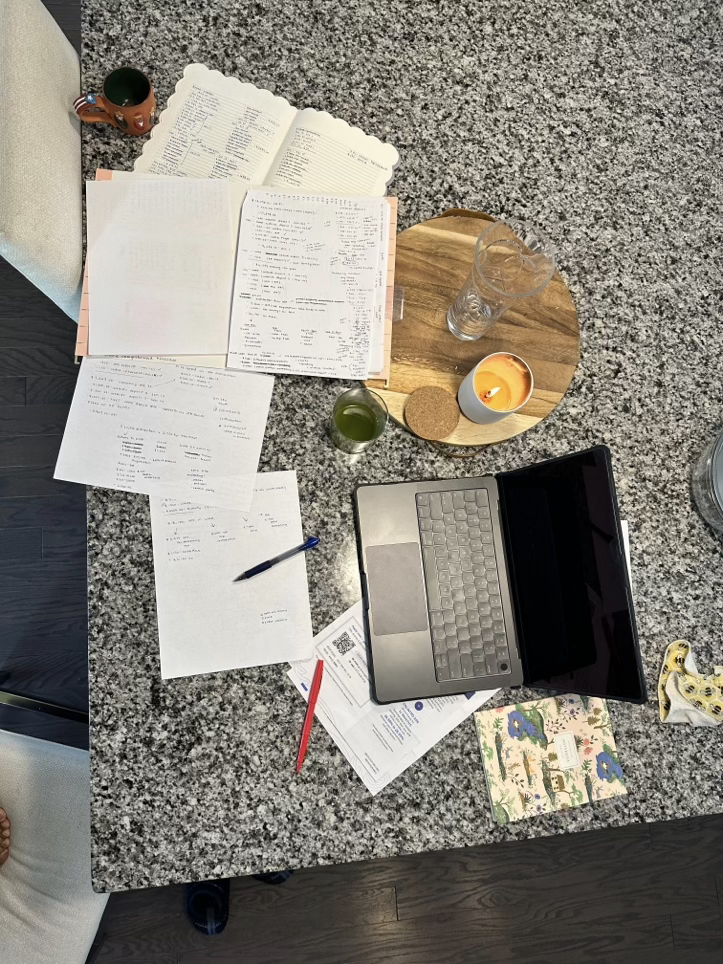

That image above is what brings me calm. Don’t get me wrong, money causes me stress. But I know that once I get the paper, pens, and plan out, I’ll find peace on the other side. Required items for every biweekly budgeting session: espresso, a lit candle, a quiet home, a planner used solely for writing out numbers, a blank sheet of computer paper, and my favorite pens. A phone or laptop must be nearby to access my banking and credit card apps.

Why do I love this method? Because it’s methodical and requires reflection.

The planner keeps a running list of recurring household expenses- what needs to be paid, the due date, and the merchant. I usually start by opening my Fidelity credit card statement, scrolling back two weeks, and checking off bills that should have auto deducted. This helps me spot changes quickly. I’ve called Verizon no fewer than five times for charging the wrong amount.

Then I manually write down all other expenses. Literally write them, pen to paper, on a blank sheet. There’s no judgment here, just observation. I total everything and make a payment for the full balance from our household checking account (where both checks get deposited, minus discretionary funds that automatically get sent to individual checking accounts).

Next, I look at what was deposited into our joint account, subtract all billed amounts, and transfer funds to savings and investment accounts. That’s it. The final step is making sure our joint account has enough to cover the next two weeks of bills. It usually does. If it doesn’t, that tells me we spent more elsewhere, the usual culprits being the dogs, travel, or random home maintenance. I don’t fret if savings must take a temporary hit, as long as the spending was intentional and I can decide whether we need to adjust the budget going forward.

So why do I have such an aversion to excel spreadsheets and budgeting apps?

Excel has never been my friend. I think some people are born with excel skills in their DNA. It’s not in mine, I’ve tried. It is in my husband’s. He loves it. Lives for it. The person that doesn’t use a mouse to navigate excel. That’s him. Budgeting in excel just doesn’t feel real to me. And budgeting apps? I get a mild form of arthritis just thinking about the hours spent categorizing six months of expenses, only to feel like the app still isn’t thinking the way I am. It can’t capture the nuances of multiple accounts or the blend between personal and household spending. And alerts on my phone don’t motivate me. Also, you have to pay for them. No thank you.

But that’s just me.

The important thing is finding a method that suits your style and sticking with it. Consistency matters far more than the tool you use. There’s no gold star for using the “most advanced” budgeting system. The best budget is the one you’ll actually return to—week after week, month after month.